The Ultimate Asset Protection Guide: Umbrella Insurance vs. LLC for Rental Properties

Owning rental property is one of the most effective ways to build long-term wealth, but it doesn’t come without its risks. Every time a new tenant signs a lease, you are exposed to potential legal liability.

Picture this: A tenant slips on an icy walkway you hadn’t cleared yet, suffering a severe spinal injury. Or, an old property you recently acquired is found to have environmental hazards that cause long-term health issues for the renting family. Suddenly, you are facing a massive lawsuit. The reality of real estate investing is that lawsuits can, and often do, exceed the standard coverage limits provided by a basic landlord insurance policy. If a judge awards a plaintiff $1.5 million and your policy only covers $500,000, your personal assets are suddenly on the chopping block to cover the difference.

Serious real estate investors know that acquiring properties is only half the battle; protecting them is the other. To shield your hard-earned assets from catastrophic legal claims, you generally have two primary options: purchasing an umbrella insurance policy or forming a Limited Liability Company (LLC).

Asset Protection Options for Landlords

While standard landlord insurance is non-negotiable, it acts as your first line of defense, offering relatively limited liability coverage. When investors look to build a fortress around their real estate portfolios, they typically turn to two established strategies:

- The Financial Shield: An Umbrella Insurance Policy

- The Legal Fortress: Forming an LLC

Both strategies protect landlords, but they do so using completely different mechanisms. An umbrella policy acts as a massive financial safety net, while an LLC creates a literal legal wall between you and your properties. Let’s break down exactly how each works so you can decide which strategy, or combination of both, is right for your portfolio.

Umbrella Insurance

What Is an Umbrella Insurance Policy?

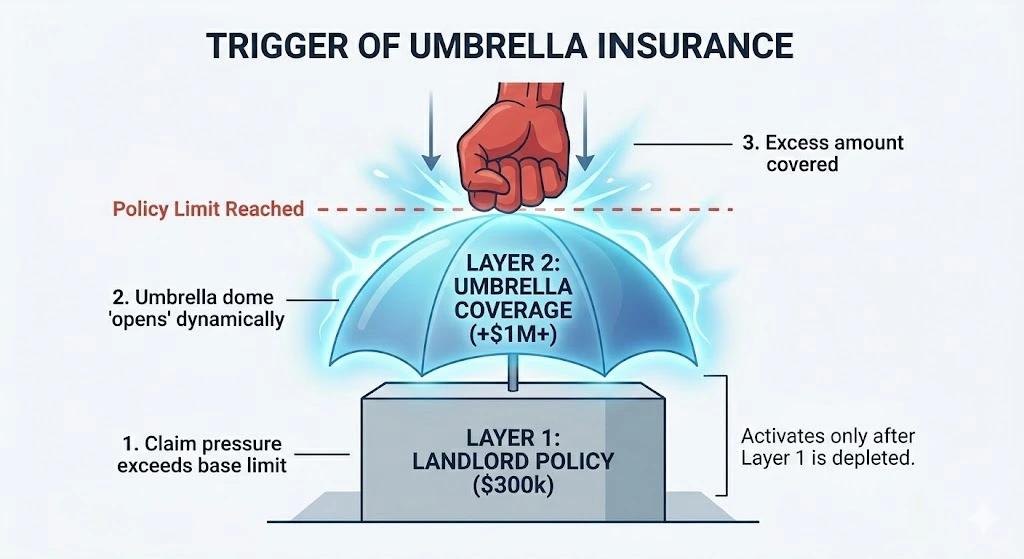

At its core, an umbrella insurance policy is extra liability coverage that sits on top of your existing primary insurance policies. It is designed to activate only after the base limits of your standard landlord insurance have been completely exhausted.

Think of it as a financial fail-safe. If your landlord policy has a liability limit of $300,000, and you are hit with a $1 million judgment because a faulty staircase led to a severe injury, your base policy pays out its $300,000 maximum. Without an umbrella policy, you are personally on the hook for the remaining $700,000. If you have a $1 million umbrella policy in place, the umbrella opens up and covers that remaining gap, keeping your personal bank accounts and primary residence safe.

The key elements of an umbrella policy include:

- Coverage Trigger: It only kicks in once primary limits are maxed out.

- Liability Extension: It dramatically increases your total liability ceiling.

- Financial Protection: It pays the settlements and judgments so you don’t have to liquidate your assets.

What Umbrella Insurance Covers

Umbrella insurance is famous for offering incredibly broad protection that goes beyond the standard perils covered by your landlord policy.

Core Coverage:

- Excess Liability Claims: Bodily injury or massive property damage claims that exceed your base policy.

- Legal Defense Costs: Lawyers are expensive. Umbrella policies often cover the exorbitant costs of defending yourself in court, sometimes outside of the policy limit.

- Medical Expenses: Coverage for severe injuries sustained by tenants or guests on your property.

Expanded Coverage:

- Slander and Libel: Protection against claims of defamation, which can occasionally arise in contentious landlord-tenant disputes or eviction proceedings.

- Emotional Distress: Lawsuits claiming psychological harm resulting from your actions or negligence as a landlord.

Cross-Policy Coverage:

One of the massive benefits of a personal umbrella policy is that it can blanket multiple areas of your life. A single policy can sit over your rental properties, your personal residence, and even your auto insurance, providing a unified liability ceiling.

Key Exclusions to Note:

- Your Own Property: It does not cover damage to the physical rental property itself (that’s what your property insurance is for).

- Criminal Acts: You are not protected if you intentionally harm someone or commit a crime.

- Certain Business Activities: Depending on the policy, large commercial real estate operations might require a specific commercial umbrella policy rather than a personal one.

The Cost of Umbrella Insurance

When optimizing cash flow, keeping expenses low is always a priority. Fortunately, umbrella insurance is widely considered one of the best bargains in the financial world.

Because the policy only triggers after your primary insurance is exhausted (meaning the insurance company’s risk of having to pay out is relatively low), the premiums are incredibly affordable.

- Typical Pricing: A standard $1 million umbrella policy usually costs between $150 and $300 per year.

- Pricing Increments: If you want to scale up, the cost per million actually decreases. Bumping your coverage to $2 million might only cost an extra $75 to $100 annually.

Pricing Factors:

The exact quote you receive will depend on a few variables:

- Property Count: The more rental doors you own, the higher the perceived risk.

- Location: Properties in highly litigious states or neighborhoods with historically high claims may bump premiums slightly.

- Underlying Limits: Insurers will require you to carry a high minimum on your base landlord policy (often $300,000 to $500,000) before they will issue an umbrella policy.

Ultimately, umbrella insurance provides millions of dollars in coverage for the cost of a few nice dinners a year.

LLC Structure

What an LLC Does for Rental Properties

A Limited Liability Company (LLC) operates on a fundamentally different principle than insurance. When you form an LLC to hold your rental property, you are creating a brand new, legally distinct entity.

Instead of John Doe owning 123 Main Street, “Main Street Holdings, LLC” owns the property. If a tenant sues the landlord, they are suing the LLC, not John Doe. This mechanism relies on a legal concept known as the “corporate veil.” The corporate veil traps the liability inside the company. If the lawsuit is successful, the plaintiff can go after the assets owned by the LLC (the rental property itself, and the LLC’s bank account), but they cannot touch your personal assets, like your primary home, your family savings, or your stock portfolio.

How LLC Protection Works

To get the full benefit of an LLC, you have to treat it like a legitimate business.

- Legal Separation: The law views you and your LLC as two different “entities.”

- Asset Isolation: If you own multiple properties and put them in separate LLCs, a lawsuit at Property A cannot easily threaten the equity you have built in Property B.

- Owner Control: As the managing member of the LLC, you retain complete control over the property, the tenants, and the cash flow, even though you don’t own the deed in your personal name.

Costs and Responsibilities of an LLC

The legal protection of an LLC is robust, but it requires significantly more administrative heavy lifting than simply paying an annual insurance premium.

Formation Costs:

- State Filing Fees: You must pay the state to form the entity, which can range from $50 to over $500 depending on where the property is located.

- Registered Agent: You are required to have a registered agent to receive legal documents, which usually costs around $100 to $300 annually.

- Legal Assistance: While you can DIY the setup, many investors pay a real estate attorney to draft a bulletproof operating agreement.

Administrative Obligations:

- Strict Financial Separation: You absolutely must maintain separate bank accounts and credit cards for the LLC. Commingling personal and business funds is the fastest way to ruin your protection.

- State Filings: Most states require annual reports and franchise taxes.

- Maintaining Formalities: You must sign leases, hire contractors, and conduct all business in the name of the LLC, not your own name.

If you fail to treat the LLC like a distinct business, say, by paying a personal utility bill out of the LLC’s checking account, a savvy lawyer can “pierce the corporate veil.” If a judge allows the veil to be pierced, your LLC protection vanishes, and your personal assets are suddenly exposed to the lawsuit.

Direct Comparison

To make the best decision for your real estate business, you have to weigh these strategies against each other.

- Protection Mechanism: Umbrella is a massive cash payout mechanism to settle lawsuits; an LLC is a legal structure that traps liability away from your personal life.

- Scope of Coverage: A single umbrella policy can cover your rentals, your personal home, and your cars. An LLC only protects the specific assets placed inside it.

- Setup and Maintenance: Umbrella insurance takes a 20-minute phone call to your broker. An LLC requires state filings, legal documents, new bank accounts, and ongoing annual compliance.

- Cost Structure: Umbrella premiums are highly predictable and generally cheap across the board. LLC costs are heavily dependent on state regulations and can be quite expensive.

- Tax Implications: Both have minimal impact on your taxes. A single-member LLC is usually treated as a “pass-through” entity by the IRS, meaning you still report the rental income on your personal tax return, exactly as you would if you just had umbrella insurance.

When Each Strategy Makes Sense

When Umbrella Insurance Is Better

Umbrella insurance is generally the superior starting point for investors in the following scenarios:

- Small Portfolios: If you only own one or two doors, the administrative hassle and cost of an LLC might outweigh the benefits.

- Desire for Simplicity: If you don’t want to juggle multiple bank accounts and annual state filings.

- High LLC Cost States: If your state charges exorbitant annual fees to maintain a corporate entity.

- Need for Fast Protection: You can get an umbrella policy bound and active within 24 hours.

When an LLC Makes More Sense

Forming an LLC becomes highly recommended, if not necessary, under these conditions:

- Large Portfolios: When you have significant equity spread across multiple properties, an LLC (or multiple LLCs) helps isolate risk.

- High Net Worth: If you have massive personal wealth outside of real estate, the corporate veil is a vital defense.

- Partnerships: If you are buying property with anyone other than a spouse, an LLC with a clear operating agreement is mandatory to dictate terms and protect all parties.

- Commercial Real Estate: Multi-family apartment complexes or commercial buildings carry inherently higher risks that demand corporate structuring.

Hybrid Strategy: The Ultimate Protection

For serious investors looking to scale, the debate between an LLC and umbrella insurance isn’t an “either/or” situation. It’s a “both/and” strategy.

The gold standard for real estate asset protection is a layered approach:

- Layer 1: Robust base primary insurance on the property.

- Layer 2: An LLC structure to separate the property from your personal assets.

- Layer 3: A commercial umbrella policy owned by the LLC.

Why this works: If the LLC gets sued for $2 million, but the LLC’s insurance only covers $500,000, the plaintiff could force the LLC to liquidate the rental property to pay the remaining $1.5 million judgment. Your personal assets are safe because of the corporate veil, but you still lose the rental property.

By having an umbrella policy inside the LLC, the insurance company writes the check for the $1.5 million judgment. You protect your personal assets, and you get to keep your cash-flowing rental property. It is the ultimate combination of legal separation and financial solvency.

Decision Framework

How do you choose the right path for your specific situation right now? Run through this quick decision checklist:

- Portfolio Size: Are you at 1 door or 10? The larger the portfolio, the more you lean toward LLCs.

- Personal Net Worth: Do you have significant personal assets that need a legal wall around them?

- Administrative Capacity: Are you organized enough to keep flawless, separate financial records? If not, an LLC could give you a false sense of security.

- State Costs: Have you looked up the exact filing fees and annual taxes for LLCs in the state where your property is located?

- Growth Plans: Do you plan to scale a massive portfolio, or just hold onto a single duplex for retirement?

Always consult with a licensed insurance broker and a qualified real estate attorney. They can review the specific data of your portfolio and recommend the exact limits and structures you need.

Conclusion

At the end of the day, neither an umbrella policy nor an LLC replaces your need for a rock-solid primary insurance policy. Choosing between an umbrella policy and an LLC depends entirely on your current portfolio size, your risk tolerance, and your willingness to handle administrative paperwork.

Start with specialized insurance for immediate, cost-effective peace of mind. As your investments grow, forming an LLC and combining it with umbrella coverage is the safest way to ensure your wealth is protected for generations.

Ready to secure your investments? Don’t leave your hard-earned assets exposed to unexpected coverage gaps. Explore your landlord and rental property insurance options with Coverlyn today, and get a tailored quote in under 5 minutes.