Short-Term Rental vs Long-Term Rental: The Complete 2026 Investor’s Guide

Real estate investing is fundamentally an exercise in capital allocation and risk management. When acquiring a residential property, you are immediately faced with a structural decision that will dictate the lifecycle of your asset: will this be a short-term rental vs long-term rental?

This is not a simple pivot you can make on a whim. The operational infrastructure, legal compliance, tax liabilities, and financing requirements for these two strategies are fundamentally opposed. Understanding the granular differences, from underwriting pro formas to IRS material participation tests, is what separates hobbyist landlords from professional investors.

Here is the definitive, data-driven breakdown of the short-term vs. long-term rental landscape, designed to help you build a profitable, risk-adjusted real estate portfolio.

The Baseline: Defining the Asset Classes

Before comparing financial returns, we must establish the precise definitions that govern how these assets are regulated, taxed, and insured.

What is a Short-Term Rental (STR)?

A short-term rental operates on a hospitality model, typically defined by guest stays of fewer than 30 days. These properties must be fully furnished down to the teaspoons and linens. Marketing relies heavily on algorithmic platforms like Airbnb, VRBO, or Booking.com. Because the asset is transient, it requires continuous high-touch management, dynamic pricing, and regular turnover.

What is a Long-Term Rental (LTR)?

A long-term rental operates on a traditional housing model, governed by established state and municipal landlord-tenant laws. Leases typically span 6 to 12 months or more, and the tenant uses the property as their legal primary residence. Properties are rented unfurnished, meaning the tenant provides their own belongings and assumes responsibility for basic interior upkeep and utility accounts.

Investment Returns: The Pro Forma Comparison

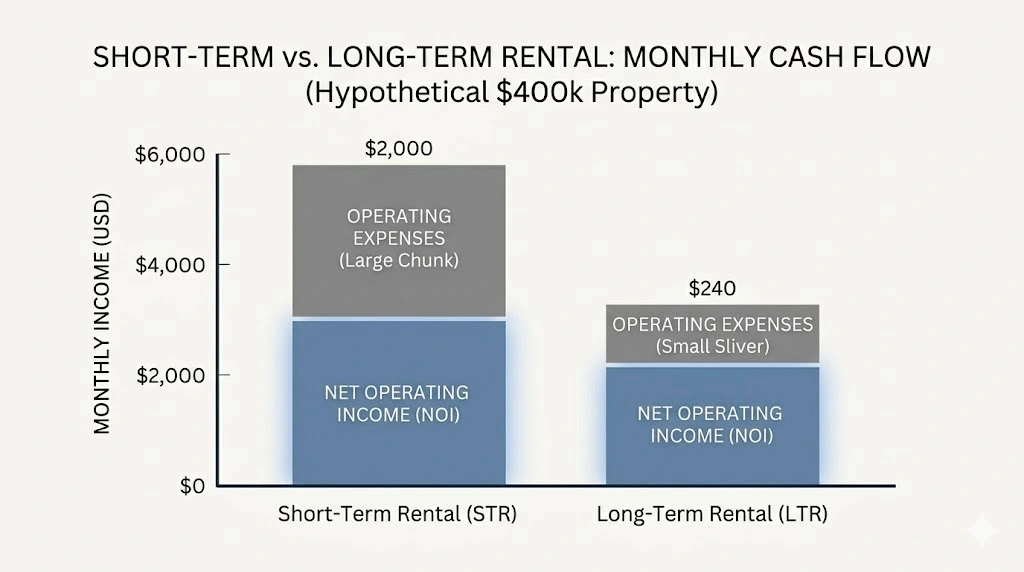

The most common question investors ask is, “Which strategy makes more money?” While short-term rentals definitively have a higher gross income ceiling, the net operating income (NOI) is heavily impacted by the expense load.

To understand the difference, we must move past generalizations and look at a mock financial pro forma for a hypothetical $400,000 property in a viable dual-strategy market.

The Short-Term Rental Math

STRs command a premium because you are selling nights, not months. Utilizing dynamic pricing, you can capitalize on weekend demand, local events, and seasonal spikes.

- Gross Revenue Projection: Assuming an Average Daily Rate (ADR) of $250 and a realistic 65% occupancy rate (approx. 20 nights booked per month), gross monthly revenue is $5,000.

- The Operating Expense Load: STRs carry heavy operational drag. You must account for cleaning fees (often passed to the guest but still a cash-flow line item), platform service fees (3–15%), full utilities, Wi-Fi, consumable restocking, and specialized commercial insurance.

- Management: If you hire a specialized STR property manager, expect to forfeit 20% to 30% of your gross revenue.

- Net Outcome: While gross revenue is double that of an LTR, operating expenses frequently consume 30% to 40% of the income, making the final cash flow higher, but vastly more volatile.

The Long-Term Rental Math

LTRs offer a lower ceiling but a highly insulated financial floor.

- Gross Revenue Projection: A standard long-term lease for this same $400,000 property might yield $2,400 per month.

- The Operating Expense Load: Because the tenant covers their own utilities, internet, and minor daily maintenance, the landlord’s variable expenses drop dramatically. Core expenses are limited to property taxes, standard landlord insurance, and capital expenditure (CapEx) reserves.

- Management: Traditional property managers charge between 8% and 10% of collected rent, a fraction of the STR cost.

- Net Outcome: The gross income is lower, but the profit margin is highly protected. An LTR might only see operating expenses consume 10% to 15% of the gross income.

The Strategy Takeaway: Use STRs to aggressively scale cash flow and accelerate ROI. Use LTRs to build a stable, predictable foundation that guarantees debt service coverage regardless of economic seasonality.

The Tax Advantage: IRS Mechanics and Depreciation

For high-income earners (such as physicians, tech executives, or business owners), the decision between a short-term rental vs long-term rental is often decided entirely by the tax code.

The Long-Term Rental Tax Limitation

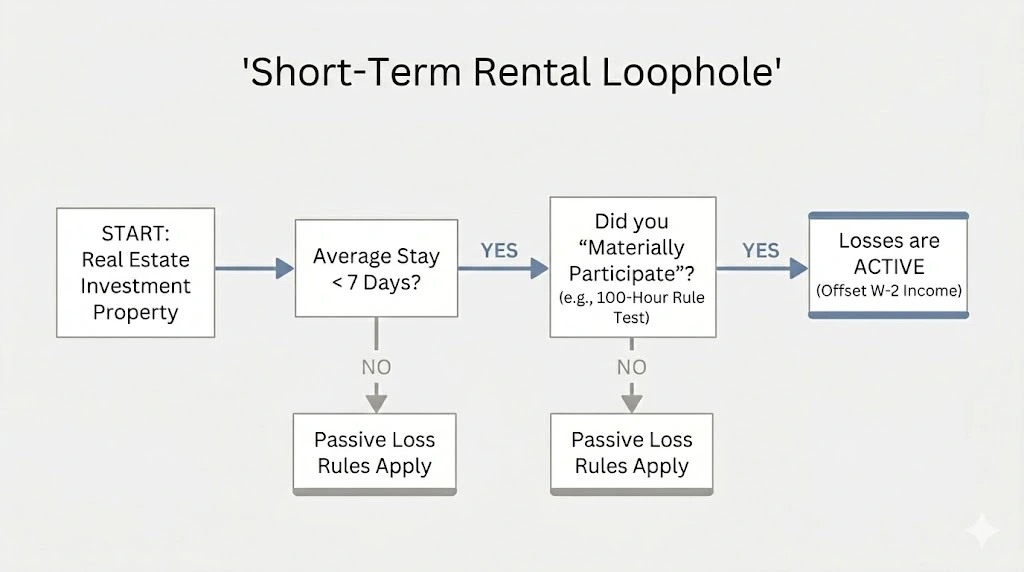

The IRS generally classifies long-term rental income as a “passive activity.” Under Section 469 of the tax code, passive losses can only be used to offset passive income. If your LTR shows a paper loss due to depreciation, you generally cannot use that loss to reduce the taxes on your active W-2 salary or business income (unless you qualify as a Real Estate Professional, which requires 750 hours of active real estate work per year).

The “Short-Term Rental Loophole”

This is where STRs provide massive leverage. If the average stay of your guests is 7 days or less, the IRS does not classify the property as a “rental activity” under the standard passive loss rules.

If you meet one of the IRS “Material Participation” tests, your STR income and losses are treated as active.

How to execute this tax strategy:

- Material Participation: The most common test investors pass is the “100-Hour Rule.” You must spend at least 100 hours managing the STR during the tax year, and that must be more time than anyone else spends on it (meaning you cannot hire a full-service property manager or let your cleaner log more hours than you).

- Cost Segregation: Investors hire an engineering firm to perform a cost segregation study, accelerating the depreciation schedule of the property’s components (like flooring, appliances, and fixtures) from 27.5 years down to 5 or 15 years.

- Bonus Depreciation: By combining active status with accelerated depreciation, an investor might generate a massive year-one paper loss (e.g., $80,000) on a profitable property, and legally use that loss to wipe out a significant portion of their W-2 tax liability.

Operational Reality: Risk, Tech, and Compliance

High returns require high sophistication. The operational gap between these two asset classes is wide, requiring entirely different tech stacks and risk management protocols.

Time Commitment and The Tech Stack

Managing an LTR requires an upfront burst of energy (leasing) followed by months of silence. Your required tech stack is minimal: a simple portal for background checks and automated ACH rent collection.

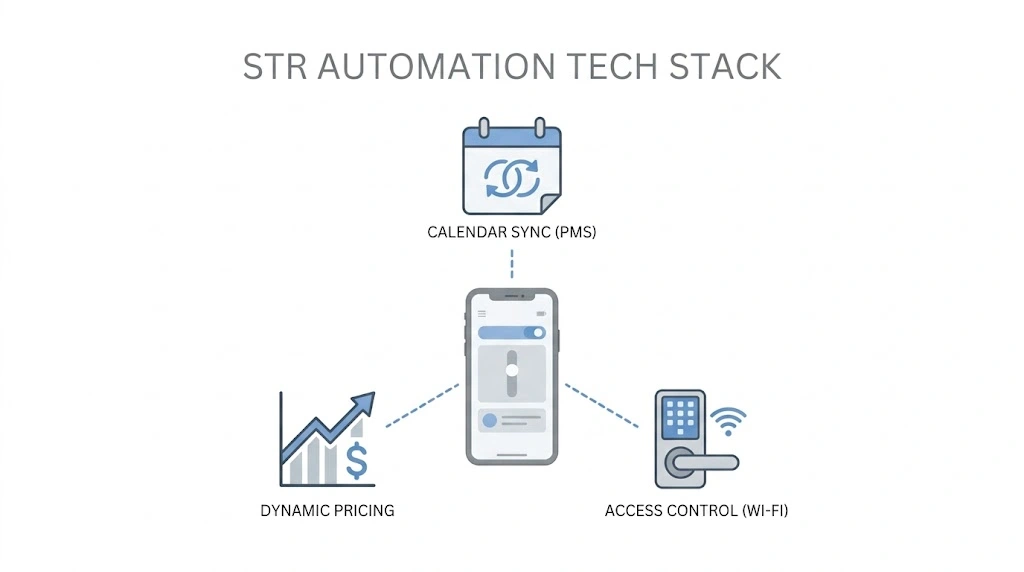

Managing an STR is a real-time logistics business. To avoid working 20 hours a week, investors must build automated systems. A standard STR tech stack requires:

- Property Management Software (PMS): To sync calendars across Airbnb, VRBO, and direct booking sites to prevent double bookings.

- Dynamic Pricing Tools: Software that analyzes local market data to adjust your nightly rates automatically based on supply, demand, and seasonality.

- Access Control: Wi-Fi-enabled smart locks that automatically generate and expire unique entry codes for each guest.

Regulatory and Compliance Risk

The largest existential threat to an STR is municipal regulation. City councils globally are aggressively restricting short-term rentals to protect local housing supplies. You could close on a property on Monday, only to have the city ban non-owner-occupied STRs on Friday.

How investors mitigate this: Modern investors do not rely on outdated zoning maps. Before underwriting a property, they integrate APIs for short-term rental compliance into their due diligence process. These data feeds automatically track shifting zoning laws, monitor local permit caps, and flag regulatory risks in real-time, ensuring you don’t purchase an asset that will become legally obsolete in six months. Long-term rentals, conversely, are entirely immune to this specific regulatory volatility.

Liability and Insurance Profiles

The liability exposure of hosting 50 different groups of strangers a year is exponentially higher than housing a single, vetted family.

- LTR Insurance: Requires a standard DP-3 Landlord policy, protecting against fire, severe weather, and basic premises liability.

- STR Insurance: Standard dwelling policies have “business pursuit” exclusions. The moment a guest pays to sleep in your house, standard coverage vanishes. STRs require specialized liability insurance designed specifically to cover transient guests, unauthorized parties, and extensive property damage.

Pros & Cons Quick Reference (With Mitigation Strategies)

Pros & Cons: Short-Term Rentals

Pros:

- Maximum Revenue: Generates 50–200% more gross income in high-demand markets.

- Active Tax Benefits: Allows W-2 earners to utilize accelerated depreciation offsets.

- Personal Use: You can block out the calendar to use the asset for personal vacations.

- Asset Condition: The property receives a professional deep clean 4 to 8 times a month, allowing you to catch maintenance issues instantly.

Cons:

- Income Volatility: High seasonal fluctuations.

- How to mitigate: Build a dedicated 3-to-6 month cash reserve funded strictly by peak-season profits.

- Regulatory Targets: High risk of changing municipal ordinances.

- How to mitigate: Only buy in cities with established, mature STR ordinances, or ensure the property’s numbers still work as an LTR as a backup plan.

- Intense Operations: Requires hospitality-level management.

- How to mitigate: Automate guest messaging and pricing, and build a localized team of trusted cleaners and handymen.

Pros & Cons: Long-Term Rentals

Pros:

- Predictable Cash Flow: Guaranteed monthly income simplifies debt service planning.

- Low Expense Ratio: Tenants cover utilities and basic upkeep.

- Passive Scalability: Easy to manage 10+ properties with minimal weekly hours.

- Favorable Financing: Banks prefer lending against traditional LTR projected income.

Cons:

- Lower Income Ceiling: Rent is capped by localized market rates.

- How to maximize: Implement “value-add” strategies, such as adding a bedroom or updating kitchens, to force appreciation and push the rent ceiling.

- Eviction Risk: Removing a non-paying tenant can take months and thousands of dollars in legal fees.

- How to mitigate: Implement a zero-exception screening standard requiring a 650+ credit score, 3x income-to-rent ratio, and pristine previous landlord references.

- Passive Tax Limits: Losses cannot easily offset active W-2 income.

The Hybrid Option: Medium-Term Rentals (MTRs)

If the operational intensity of an STR sounds exhausting, but the low returns of an LTR sound uninspiring, there is a highly lucrative middle ground: The Medium-Term Rental.

MTRs cater to stays of 30 to 90 days. The target demographic includes traveling nurses, corporate relocations, digital nomads, and families displaced by home renovations.

Why it works: You furnish the property exactly like an STR and can charge a premium rent (often 1.5x to 2x standard LTR rates). However, because the stay exceeds 30 days, you largely bypass municipal STR bans and hotel taxes. Furthermore, your turnover rate drops from eight times a month to just four times a year, massively reducing your operational headache and cleaning costs.

Decision Framework: Which Strategy Fits Your Profile?

The “best” real estate strategy is entirely subjective. It depends on your current tax bracket, free time, and psychological tolerance for risk.

Execute a Short-Term Rental Strategy if:

- You are a high W-2 earner specifically seeking to leverage the material participation tax loophole.

- You have the capital to absorb a slow booking month without panicking.

- You are willing to treat the investment as an active hospitality business, not a passive bond.

- You are buying in a verified destination market (beaches, mountains, major event hubs).

Execute a Long-Term Rental Strategy if:

- Your primary goal is slow, steady wealth preservation and debt paydown.

- You work 50+ hours a week and need an investment that does not ping your phone on a Saturday night.

- Your target market has weak tourism metrics but strong population and job growth.

- You are prioritizing the rapid scaling of a large unit-count portfolio.

The Execution Checklist

Once you have chosen your path, execution is everything. Follow these critical steps to launch your asset securely.

- Data-Driven Market Research: Stop guessing. Use real estate analytics platforms to pull hard data. If analyzing STRs, look at historical ADRs, seasonality trends, and local permit availability. For LTRs, analyze localized job growth, school district ratings, and vacancy rates.

- Stress-Test the Underwriting: Build a pro forma that accounts for worst-case scenarios. Can the STR survive a 40% occupancy winter? Can the LTR survive a two-month eviction vacancy? Always build a capital expenditure (CapEx) reserve into your monthly math.

- Establish Legal Infrastructure: For STRs, apply for your municipal permits and set up your dynamic pricing tech stack. For LTRs, consult a local real estate attorney to draft a landlord-tenant compliant lease that protects your rights.

The Bottom Line

Both short-term and long-term rentals are proven vehicles for building generational wealth. The short-term rental offers aggressive cash flow and elite tax optimization at the cost of your time and elevated risk. The long-term rental offers psychological peace, stability, and passive equity growth at the cost of maximum immediate revenue.

Do not force a strategy onto the wrong market, and do not force an active hospitality business onto a passive investor mindset. Choose the path that aligns with your capital, protect it with the right data and insurance, and execute.

Secure Specialized Insurance to Protect Your Investment

When it comes to insurance, it is crucial that you secure coverage built for your exact strategy. This is where Coverlyn comes in. As a dedicated landlord insurance platform (and a subsidiary of Mashvisor), Coverlyn provides comprehensive coverage built specifically for the unique risks of rental property owners.

Whether you need protection against guest-caused property damage, liability, theft, or weather-related events, Coverlyn offers specialized policies and instant online quotes so you can protect your investment with ease and confidence.