Rental Property Insurance: A Simple Guide to Landlord Insurance

Landlords need proper rental property insurance to safeguard their real estate investment and income. With so many options available on the market, beginners find it difficult to get started and find the best policy.

Getting the right coverage requires a few steps. First, you need to know the difference between homeowners insurance and landlord insurance and how it applies to rentals. Second, you have to evaluate the specific risks and threats pertinent to your market and property type.

After you’ve identified the type of insurance that your situation renders, you should compare a number of insurance companies, the policies they offer, and the prices they charge. Finally, you need to take into account all insurance costs, such as premiums and deductibles, to make the best decision for your investment business.

Homeowners Insurance vs Landlord Insurance: What’s Different

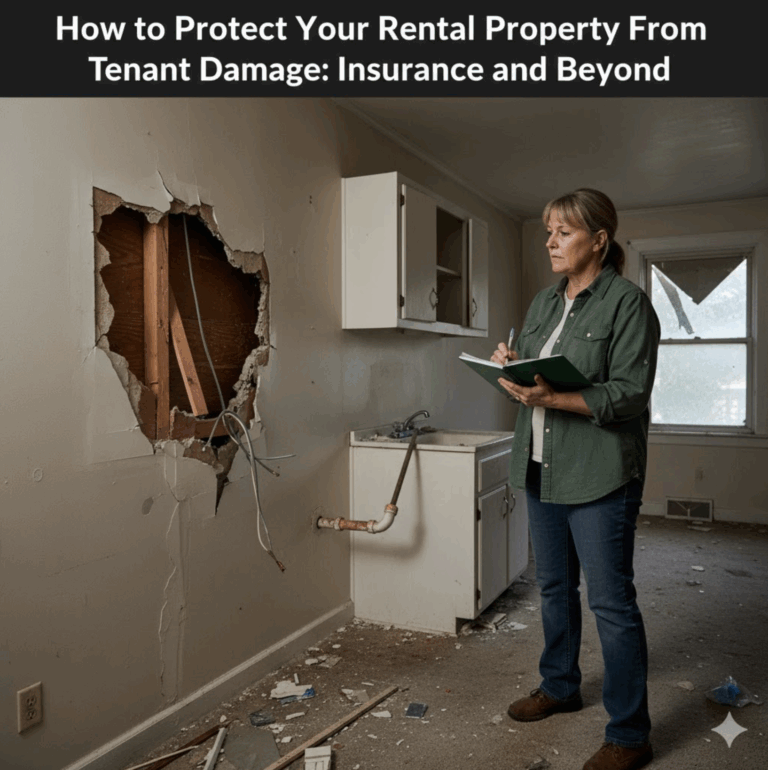

While rental property insurance is not required by law in the US market, statistics show that the majority of real estate investors get a separate policy for their investment property. The most frequent claims on these policies include water damage, storm damage, unintentional damage by a tenant, liability issues, and loss of rental income. But the truth of the matter is that this insurance can protect you against a range of risks.

The reason for the need for specialized insurance for landlords is that it is different from homeowners insurance and covers different events. Landlord insurance policy responds to the unique protection needs of rental properties and their owners. Specifically, it covers both the property’s physical structure (the building itself) and the personal belongings of the landlord used in rental activities (furniture, appliances, valuables, etc.). It also offers coverage against liability and some other inherent risks that investors face.

Meanwhile, homeowners insurance is meant to be used for primary residences, or homes inhibited by the owner. As such, it doesn’t protect against the specific dangers and threats that landlords experience. Most importantly, homeowners insurance for rental property doesn’t reimburse for damage caused by non-owner tenants.

The table below provides a side-by-side comparison of the homeowners and rental property insurance and what one each one covers:

Homeowners Insurance vs Landlord Insurance

| Coverage | Homeowners Insurance | Landlord Insurance |

| Property Damage | ✅ | ✅ |

| Personal Property | ✅ | Only if used in rental activities |

| Personal Liability | ✅ | ✅ |

| Rental Income Loss | ❌ | ✅ |

| Additional Living Expenses | ✅ | ❌ |

| Medical Payments | ✅ | ❌ |

| Ordinance/Law | ❌ | ✅ |

Note: The table above summarizes the common provisions of the homeowner’s vs landlord insurance. However, there might be variations in coverage by state and insurance company. That’s why before choosing a policy, it’s important to research different insurance providers and consult with an insurance agent to understand what coverage you’re getting.

Property Risk Assessment

To select the right rental property insurance for your situation, the first step is to evaluate the needs and requirements of your property including:

- Location

- Age

- Condition

- Additional structures and amenities

- Target tenants

When assessing the market-related risks, take into account the impact of environmental factors, such as drought, wild fires, desertification, and air pollution. Knowing the exact risks to which your investment property is exposed will help you decide on the policy that’s best fit so that you strike the right balance between coverage and cost.

Next, you have to do due diligence by studying and comparing a number of landlord insurance policies offered by different companies. Focus your research on the amount and type of protection that your property requires.

Since there are so many environmental factors that might affect your rental property and the seriousness of many of them changes over time, it’s usually a good idea to use professional tools to evaluate risks in a particular geographical area. Such tools consider climate, zoning, building codes, and other information metrics for comprehensive assessment of investment risk.

Policies Comparison

A common mistake beginner landlords make is to get the first insurance that comes their way. Actually, it’s important to investigate different options, considering both large, national insurance companies and small, local providers to get the best value money. It’s one of your core responsibilities to get proper protection for your investment while also keeping cost reasonable as it impacts overall profitability.

Premiums and Deductibles Considerations

Your selection of the right policy should be partially guided by the landlord insurance cost. After all, the insurance cost turns into a recurring expense in your budget as an investor.

There are two main components that comprise the cost of insurance for rental property:

Premiums

The first element of the rental property insurance cost is the premium. The insurance premium is the amount of money you need to keep paying on a regular basis to maintain your selected level of protection. Payments are typically made monthly, quarterly, or annually.

The main factors that determine premium include:

- Type and amount of coverage

- Cost to replace property

- Location

For instance, properties located in high-risk areas – with a high rate of natural disasters or crime – demand higher premiums. Similarly, the landlords of more luxury homes with more expensive furnishing and appliances pay more to insure their property.

Deductibles

The second major component of rental insurance cost is the deductible. This refers to the amount of out-of-pocket money you have to pay yourself after a covered incident before the insurance company starts compensating you.

For example, if your deductible is $2,000, and the covered loss is $15,000, you’ll cover the pay $2,000 and the insurance provider will provide the remaining $13,000.

When choosing deductibles, keep in mind that a higher deductible might help you bring down the premium, but you’ll have to spend more in case of a covered event. It’s all about striking the right balance.

Keeping Your Rental Property Insurance Up to Date

Getting a rental property insurance policy is not a one-time deal. You should periodically review your current policy vis-a-vis potential changes in your situation as a landlord to ensure that your investment assets remain properly protected. For example, a recently upgraded rental with a remodeled kitchen and newly added amenities might require higher insurance coverage to remain adequately taken care of.

Similarly, when the time to renew your policy approaches, it is a good idea to talk to a few insurance companies to compare rates. It might be that your provider raised prices over the course of the year, while others brought them down, so your policy is no longer competitive. Also, there’s no harm in trying to negotiate better terms and lower premiums to optimize value.

Bottom line: Getting the best insurance for your investment property boils down to 1) understanding the difference between homeowner’s insurance vs landlord insurance and why you need the latter, 2) carefully evaluating risks, and 3) juxtaposing insurance policy and cost options from a number of companies. Finally, remember to frequently review your insurance to keep your rental property well protected.