How Is Rental Income Taxed? The Ultimate Guide for Landlords

When you first become a real estate investor, the concept of rental income seems incredibly straightforward: your tenant writes you a check, and you put it in the bank.

But in the eyes of the IRS, rental income is far more nuanced. Depending on how you receive it, when you receive it, and what services you provide, the way your revenue is classified and taxed can change drastically. Whether you are planning to buy your first investment property or you already manage a growing portfolio, understanding the tax mechanics behind your rental business is critical to maximizing your profits.

In this guide, we’ll break down exactly what the IRS considers rental income, how it gets taxed at the federal and state levels, the unique rules for short-term rentals, and the strategies savvy investors use to optimize their tax returns.

What Actually Counts as Rental Income?

At its core, the IRS defines rental income as any payment you receive for the use or occupation of your property. If a value comes to you because you own the property, it’s safe to assume the IRS wants to know about it.

Here is how different types of payments are classified:

- Monthly Rent: The standard, recurring payments your tenants make. This is always taxable as ordinary income in the year you receive it.

- Advance Rent: If a tenant pays for the last month’s rent when they move in, that money is taxed in the year you receive it, not the year it applies to.

- Security Deposits: A security deposit is not considered taxable income when you collect it, provided you plan to return it. However, if you keep a portion of the deposit to cover unpaid rent or repair damages beyond normal wear and tear, that retained amount becomes taxable income in that year.

- Tenant-Paid Expenses: If your tenant pays a bill that is technically your responsibility (like a water bill or a property tax installment) in lieu of rent, that amount must be reported as rental income. You can, however, usually deduct that expense later.

- Services in Exchange for Rent: If a tenant paints the house in exchange for a free month of rent, you must report the fair market value of that month’s rent as income.

- Lease Cancellation Payments: If a tenant pays you a fee to break their lease early, those funds are taxable in the year you receive them.

How Rental Income Is Taxed (Federal Level)

Rental income is generally classified as ordinary income. However, the beauty of real estate investing lies in the fact that you are taxed on your net rental income, not your gross receipts.

Net Rental Income = Total Rental Income – Allowable Deductions

Federal Reporting Mechanics

For most individual landlords, rental income is reported on Schedule E of your Form 1040. Because it is treated as ordinary income, your net rental profits are taxed according to your standard federal income tax bracket, which ranges from 10% to 37%.

The Power of Deductions

The secret to real estate wealth is that many landlords legally reduce their taxable rental income to zero (or even claim a loss) through heavy deductions. Major deductible categories include:

- Mortgage Interest: One of the largest deductions for leveraged investors.

- Property Taxes: State and local taxes assessed on the property.

- Operating Expenses: Insurance, property management fees, maintenance, utilities, and marketing.

- Depreciation: The IRS allows you to deduct the cost of the physical structure (not the land) over 27.5 years for residential property. This “phantom expense” shields a massive portion of your cash flow from taxes.

- Professional Services: Fees paid to lawyers, accountants, or tax advisors.

1099 Forms & the Reality of Reporting

Unlike a standard W-2 job, no one is automatically withholding taxes from your rental checks. Tenants do not issue you a 1099 form, meaning the obligation to accurately self-report your income falls entirely on you.

However, if you use a property management company or collect rent through third-party payment processors, you might receive a Form 1099-K. While the IRS previously planned to drastically lower the reporting thresholds, recent tax legislation passed in 2025 permanently restored the original limits. Today, payment processors are only required to issue a 1099-K if you receive over $20,000 in gross payments AND have more than 200 transactions in a single year. Keep in mind that even if you don’t meet this threshold and don’t receive a 1099-K, every dollar of rental income must still be reported to the IRS.

State Income Tax Treatment

While federal tax rules apply to everyone, your state tax burden depends entirely on geography.

The Property Location Rule

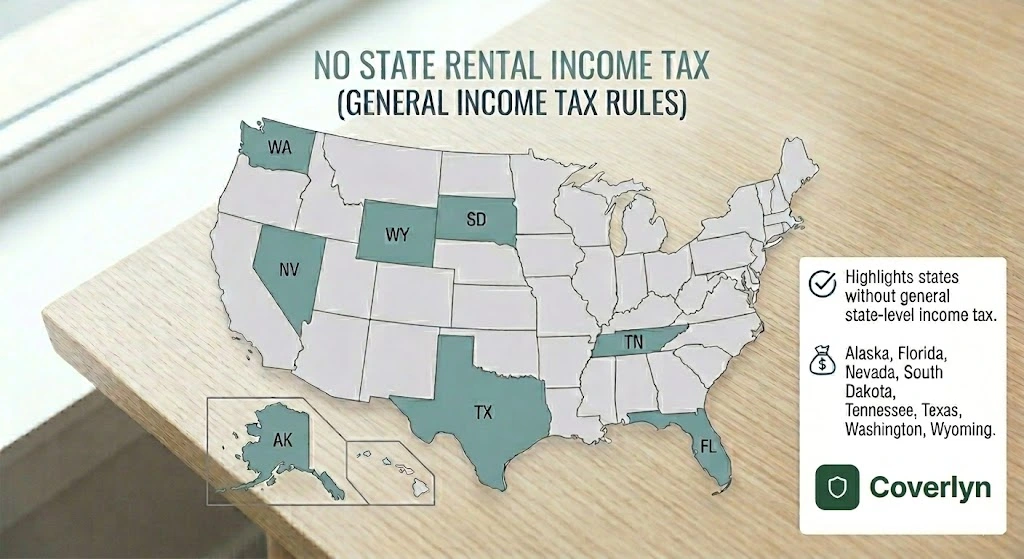

The golden rule of state taxes is that the state where the property is located gets to tax the income generated there. If you live in New York but own a rental in Florida, Florida’s tax laws apply to that property’s income.

- No-Income-Tax States: Investing in states like Texas, Florida, Nevada, Tennessee, South Dakota, Alaska, Washington, and Wyoming means you won’t pay state income tax on your rental profits. (Note: New Hampshire only taxes interest and dividends).

- High-Tax States: Properties in states like California or New York will face state-level income taxes on top of federal brackets.

Keep in mind that states with no income tax often compensate with higher property taxes or specialized insurance requirements, so you must evaluate the entire financial picture.

The Short-Term Rental Difference (Airbnb / VRBO)

Short-term rentals (STRs) play by a slightly different set of tax rules than traditional long-term leases.

- The 14-Day Rule (The Augusta Rule): If you rent out your personal residence for 14 days or fewer out of the year, you do not have to report the rental income. It is entirely tax-free. However, you also cannot deduct any rental expenses.

- Active vs. Passive Classification: If you provide “substantial services” to your STR guests, like daily maid service, fresh linens, or breakfast, the IRS may view your property as a hotel business. This means your income gets reported on Schedule C and is subject to self-employment taxes (FICA). If you don’t provide these hotel-like services, it remains passive income on Schedule E.

- Occupancy Taxes: Many municipalities require STR owners to collect local hotel or occupancy taxes. If the platform (like Airbnb) collects and remits this on your behalf, it is generally treated as a pass-through and isn’t counted as your rental income.

Strategies for Maximizing Tax Benefits

To make the most of real estate’s incredible tax advantages, you need to be proactive.

- Keep Pristine Records: Maintain a dedicated, separate bank account for every rental property. Commingling personal and business funds is a fast track to an IRS headache.

- Understand Repairs vs. Improvements: A repair (fixing a leaky pipe) can be fully deducted in the current tax year. An improvement (putting on a brand new roof) must be capitalized and depreciated over several years.

- Explore Cost Segregation: For larger properties or high-income earners, a cost segregation study allows you to accelerate the depreciation of certain property components (like appliances or flooring) to get massive tax write-offs upfront.

- Leverage Passive Activity Loss Rules: Generally, passive rental losses can’t offset active income (like your W-2 salary). However, if your Modified Adjusted Gross Income (MAGI) is under $100,000, you may be able to deduct up to $25,000 in rental losses against your active income.

- Hire a Real Estate CPA: The tax code is complex. A qualified tax professional will pay for themselves by finding deductions you missed and keeping you compliant.

The Bottom Line

Rental income encompasses any value you receive from your property, and while it’s taxed as ordinary income, the federal tax code heavily favors real estate investors through deductions and depreciation. By understanding state-level variations, short-term rental nuances, and the power of strategic tax planning, you can legally keep more of your hard-earned cash flow.

Protect Your Rental Income with Coverlyn

You’ve optimized your tax strategy, now it’s time to protect the property that generates your income. Coverlyn provides comprehensive landlord insurance designed specifically for property investors.

Whether you’re guarding against water damage, fires, or tenant-related liability claims, we make coverage simple and accessible across all 50 states. Join over 10,000 property owners who trust Coverlyn to safeguard their investments.